Overview

The university generally plans to break even on recurrent activities of the core university, not earning a profit or a loss. Budgets in 2014/15 were taken as a baseline for each unit, with formulaic changes calculated each year. The baseline, adjusted by formulaic changes, is communicated as the Budget Targets for each unit each year. The Budget Targets represent the full allocation of planned income, i.e. planned expenditure matching planned income.

Additional Resources

For the university, the principal sources of unrestricted income for recurrent activities are State Grant Income and Fee Income. As is widely acknowledged, the current levels of State Grant Income are inadequate. Until there is a clear basis for expecting meaningful real increases in grant income, we budget on the basis of the grant remaining constant in real terms (i.e. matching the cost of pay rate increases of staff designated as Core-Funded under the Employment Control Framework).

The principal source of additional income to the university therefore is Fee Income. If we earn additional fee income we have scope for allocating additional resources; unless we earn additional fee income we don't have scope for allocating additional resources.

Research Income (whether direct or indirect) is restricted and subject to the rules of the funding agency. As such, research income and research expenditure are generally seen as operating side-by-side with the UCD Financial Model rather than being a component part.

Fee Income Incentivisation

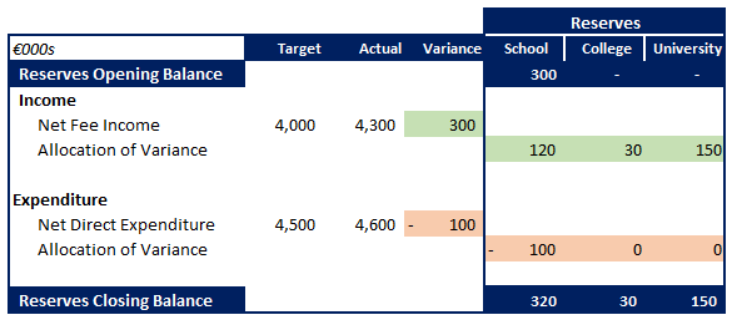

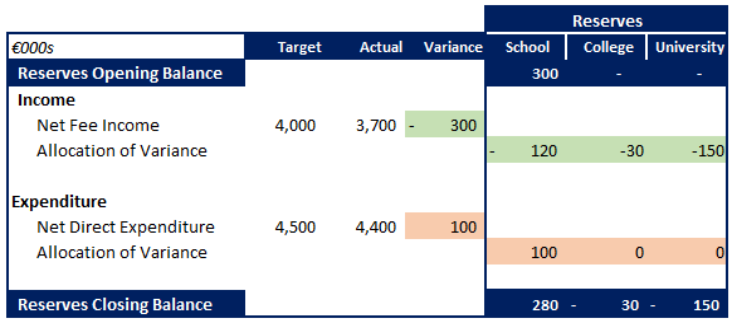

Resources associated with additional Net Fee Income versus Budget Target are shared on a formulaic basis, providing clear incentives and expectations to schools. Because additional Net Fee Income leads to additional resources for a unit, the incentivisation is also called Performance Based Funding.

50% of net additional fee income is allocated to local units (school and college) and 50% to the university.

An individual school will receive 40% of its net additional fee income formulaically. 10% of the additional funding is allocated to the college, but the Principal may waive some or all of this in favour of the school, or may use it for the collective benefit of the schools in the college.

50% of net additional fee income is allocated to the university's Performance Based Fund formulaically. Distributions from this fund are made to academic and support units and for institutional purposes on a discretionary basis.

Discretionary Reserves

Performance Based Funding and Net Direct Expenditure variances at year end are placed in reserve accounts for each unit. These accounts are described as Discretionary Reserves because the funds contained may be used at the unit's discretion.

Normally they will be used on a planned basis as identified during the planning cycle. Such reserves might provide an opportunity to spend in excess of the normal recurrent budget level, for example while a new program is being established, or to enable recurrent expenditure to be maintained even if there are temporary shortfalls in fee income. Sustainability is the key element of Five Year Plans - discretionary reserves can be used to smooth out peaks and troughs, but do not allow a unit to proceed on an unsustainable path.