The planning horizon for strategic plans will be the 5 years to 2030

FAQs - Strategic Planning

Plans should be as concise as possible. If possible, use bullet points rather than long paragraphs. We want to make the process as easy and user friendly as possible.

All of our strategies and plans should reflect the priorities identified in overview. Schools and units should develop their plans for the 5 years to 2030. While this may not represent fundamental changes from plans developed last year, it is appropriate to re-consider all aspects of the plans in the light of our themes, objectives and enablers and how these impact on your school or unit.

Your first point of contact should be your College Principal or Vice-President. Your local Finance Manager will also provide help and support throughout the process.

Additionally, Sarah O'Flaherty would be delighted to meet with you at any point in the process to discuss any issues you may have.

Yes, very much so!! The areas where you plan to invest over the coming years are an essential element of the plan.

FAQs - Financial Planning

The current Targets act as the base for setting new Targets, with standard adjustments applied as below.

Fee Income Target

| Element | Explanation |

| Base Net Fee Income Target | The Target for the current year is the starting point in setting the Target for the new year. |

| Adjustment regarding Current Year Net Fee Income | If Net Fee Income is expected to match Target for this year, no adjustment to the Base Net Fee Income Target is required. If the Net Fee Income earned this year is higher than this year's Target, then a favourable variance will occur and the school will receive Performance Based Funding to increase its Reserves. In most cases, schools plan on maintaining the higher level of fee income and wish to spend the associated Performance Based Funding. Therefore an adjustment is applied to the Base Net Fee Income to bring it up to the level of Current Year Net Fee Income, and the Net Direct Expenditure Target is also increased. If a school does not expect the higher level of fee income to be maintained, it may request that the adjustment be reduced or removed, once the initial Target has been issued. The Net Direct Expenditure Target will also be adjusted, in proportion. If the Net Fee Income earned this year is lower than this year's Target, then an unfavourable variance will occur and a charge against the school's Reserves will be made. In most cases the school will aim to put in place measures to restore the lost fee income and so no adjustment to the Current Year Target is applied when setting Targets. If a school does not believe that the Target is achievable, it may request an adjustment to be applied, once the initial Target has been issued. The Net Direct Expenditure Target will also be adjusted, in proportion. |

| Net Fee Income Target | The Base Target plus or minus the Adjustment equals the Net Fee Income Target. |

Net Direct Expenditure Target

| Element | Explanation |

| Base Net Direct Expenditure Target | The Target for the current year is the starting point in setting the Target for the new year. |

| Adjustment regarding Current Year Net Fee Income - Unit Share | As discussed above, there may be an adjustment to the Net Fee Income Target to reflect the Current Year's actual Fee Income. If so, there is a proportional adjustment to the Net Direct Expenditure Target. If the Net Fee Income Target is increased, then the Net Direct Expenditure Target is also increased; if the Net Fee Income Target is decreased, then the Net Direct Expenditure Target is also decreased. |

| Adjustment regarding Pay Rates | If the State has approved pay rate increases for the coming year, then Budget Targets are adjusted accordingly as set out below, depending on whether the faculty/staff are designated under the ECF as being Core Funded or Non-Core Funded and whether the unit is an Academic Unit or not. ECF Core Funded Faculty/Staff Net Direct Expenditure Target increases to match the pay rate increases are applied for all types of unit. ECF Non-Core Funded Faculty/Staff Academic Units are expected to avail of the Performance Based Funding mechanism to generate the funding required to cover these costs and so no adjustment is made. Admin units within the Colleges are expected to utilise their share of Performance Based Funding to cover these costs, and therefore no adjustment is made. Support Areas and Research Institutes do not earn Fee Income and so are not in a position to earn Performance Based Funding. Therefore the increased costs are covered by an increase to the Target. A small number of units in Support Areas (e.g. Applied Language Centre) do come under the Performance Based Funding mechanism and therefore do not receive a Target adjustment for these costs. |

| Mainstreaming Adjustment | In a small number of cases where units are in receipt of central income annually, it may be appropriate to 'mainstream' the funding into the budget i.e. increase the Target and cease transferring the income. This is neutral overall and can be seen as an accounting adjustment that does not affect the real budget level. The Finance Office will agree any such mainstreaming with the relevant Head. |

| Net Direct Expenditure Target | The Underlying Base Target plus or minus the Adjustments above equals the Net Direct Expenditure. |

The charge for Social Costs will be 1.0% for the Research Social Cost Fund & the Main Social Costs Fund.

Further information about the Social Costs Fund is available on the Finance Office website.

ECF targets will be updated to reflect the latest targets provided by HR.

No - the university's share of additional fee income is placed in the University Performance Based Fund (UPBF). In the early years of the fund, applications for disbursements from the Fund were invited. Some of the disbursements were once-off but many were ongoing or multiannual and so are still being funded. The fund is now pre-committed for strategic purposes including the Central Pool Academic Appointments and other enablers of the university strategy. Accordingly there will be no call for funding from the University Performance Based Fund or the UPBF-Minor Works Fund.

Central Pool Academic Appointments should be included in the Staff Plan where an appointment has been made, even if the appointee has not yet commenced.

As schools will receive income for the positions from the university, they are included at 0 cost in school plans. The FTE should be included in the local staff plan.

Potential future appointees in future years should not be included.

Central Pool Academic Appointments are expected to address the Student/Faculty ratio rather than directly add to capacity and so should not be an integral part of additional income generation plans.

In reality, the average Fee Income for a programme is usually a little bit different to the published fee rate because of circumstances such as students dropping out, students taking more or less than the standard number of credits etc. When planning future fee income we use the average rate rather than the formal published rate, and we use separate averages for EU and NonEU.

Fee Income in the Base Five Year Plan is generated from the most recent census in the current year and so uses current year fee rates. Approved fee rate increases for 2025/26 have been applied in PBCS. No further increases should be applied in future years.

Next year's pay rate increases are known with a degree of certainty and will be used in the costing of staff plans.

Given the difficulty in comparing financial numbers that include cumulative inflation, we perform our financial planning using constant rates for both costs and income. These rates are set as per next year i.e. 2025/26, with no further increases.

The State is providing additional funding to the higher education sector via the Human Capital Initiative. Information on the initiative is available from the (opens in a new window)HEA website. Funding is coming from the National Training Fund (NTF) and the initiative is focused on skills-focused programmes designed to meet priority skills needs.

The HEA has set conditions regarding how funding is used and these do not match with the standard UCD Financial Model. As these conditions are set by the funder, they will take precedence over UCD's own model. Broadly the 2 overarching conditions are

- It is expected that the majority of additional places funding is targeted at the enhancement and benefit of the Dept/School where the additional places are being hosted and this should be reflected in the funding financial monitoring reports;

- Overheads will be a max 20% of direct costs excluding equipment and additional places.

The additional funding for additional places will be treated in UCD as Earmarked Grant funding and will be transferred in full to the relevant school(s);

The 20% overhead funding will accrue to the university.

Full details of the Ad Astra Fellow Performance Assessment process is set out on the HR website:

Each unit should assume no change in the energy cost rate from Estates. If units are anticipating any notable changes in usage through on-going projects or initiatives, these should be factored into the overall cost movement.

FAQs - Research Planning

While there are some measures of quality that try to by broadly applicable (e.g. Field Weighted Citation Impact), there will generally be discipline specific approaches needed to truly evaluate quality. A general view would be that high quality research would be recognised as excellent by peers in other institutions. The UCD quality framework https://www.ucd.ie/quality/

This measures any relevant research output that can be captured in UCD’s Research Funding System (RFS) and/or major publication databases such as Scopus and the Web of Science.

We recognise that impact has academic, societal and economic elements, defined as follows:

Academic impact is the demonstrable contribution that excellent research makes to academic advances, across and within disciplines, including significant advances in understanding, method, theory and application.

Societal and economic impact is the demonstrable contribution that excellent research makes to society and the economy, of benefit to individuals, organisations and nations.

https://www.ucd.ie/

It is entirely natural for research ideas and ambitions to come from individuals, groups and centres. However if there is no coordination at a school level then there can be unwanted duplication and fragmentation of activity. Furthermore, finite school resources such as space, administrative support, overhead investment and other financial support could inadvertently be stretched too far by these competing plans if there is no plan at a school level.

UCD research institutes typically facilitate and support research across multiple schools, therefore no institute plan would entirely align with any given school. Schools should engage with the relevant Institute Directors as part of the planning process to understand what the institutes provide already and how that can link to the school’s plans.

Different research funders provide different levels of overhead return based on your expenditure on the research activity in a given year. Therefore the amount of overhead generated at the end of the year depends on the amount (and type) of actual research expenditure during the year. A set percentage of this is returned to schools, which is increasing year on year until it reaches 40%. Large funded research programmes such as SFI Centres have particular associated costs which must use some of that returned overhead.

The Head of School is overall responsible for the school plan, which includes a section on research. However there are other important roles to support this. Many schools have an associate dean or director of research who can facilitate internal school discussion and analysis of research, and provide insight to the development of the research plan. Furthermore Lead PIs of relevant research centres (e.g. SFI Centres) or Directors of UCD Institutes can provide insight on the school’s research activity in those entities, and highlight opportunities for future participation (details available here: https://www.ucd.ie/research/

The College VP for Research and Innovation (VPRI) should liaise between the schools of the college to look at opportunities for relevant collaboration and cooperation across the college.

Your college Research Partner can provide support and advice (list here https://www.ucd.ie/research/

FAQs - Planning Documents

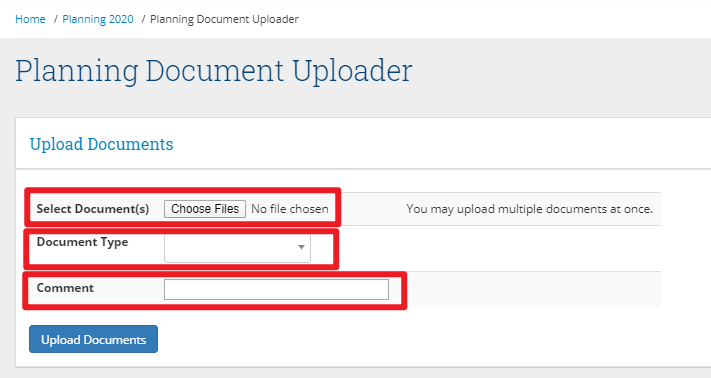

Within the (opens in a new window)InfoHub / Finance / Planning Documents screen, click on the Document Uploader button to upload documents.

The Document Uploader enables the user to select one or more files from their computer or other device, to select a Document Type (i.e. Category), and to provide an optional comment before uploading. The Document Type for the submission is Submission by School or Unit.