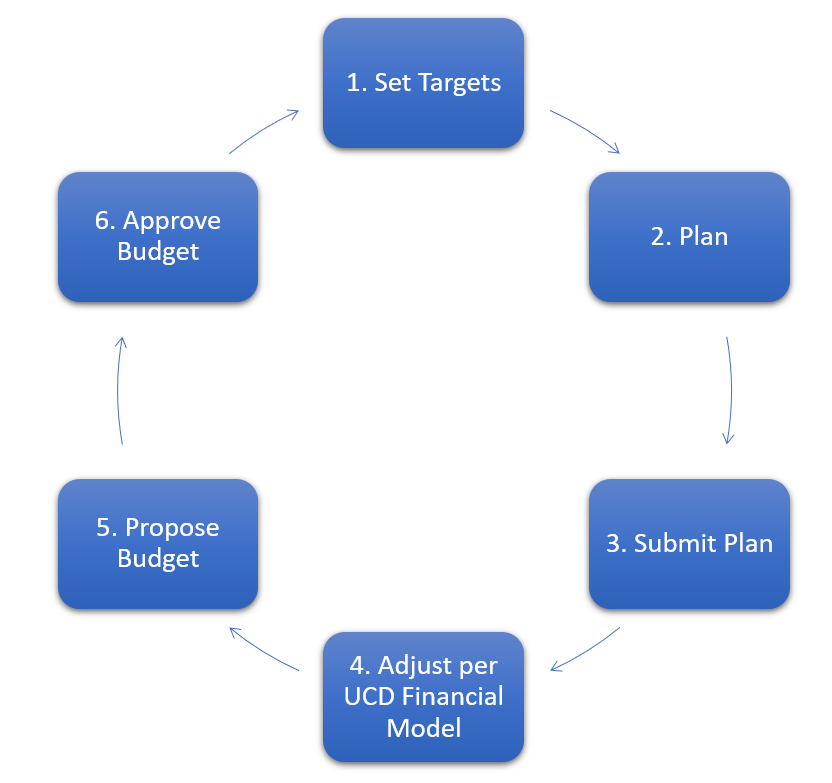

Each year the Budget Approval process starts by setting Targets based on the prior year's Target, with adjustments in accordance with the UCD Financial Model. Plans are then developed for each unit, submitted and the first year of the plan is approved as the Budget.