The relationship between climate change and agriculture is a contentious, complex and important one. In this series of twelve blogs, UCD Adjunct Professor Frank Convery will explore the context, challenges and potential solutions for dairy, beef and sheep farming in Ireland. Each blog presents key evidence to underpin informed debate and the series seeks to help plot a sustainable future for the sector.

Professor Tasman Crowe, Director, UCD Earth Institute

7. Climate Performance by Irish Ruminant Farming: New Zealand Climate Policy for Agriculture Forestry and Land Use (AFOLU)

Frank Convery, Adjunct Professor, University College Dublin

How to cite this blog (APA): Convery, F. (2023, January 27). Climate Performace by Irish Ruminant Farming: New Zealand Climate Policy for Agriculture Forestry and Land Use (AFOLU). UCD Earth Institute Climate Policy for Ruminant Agriculture in Ireland. https://www.ucd.ie/earth/newsevents/climate-policy-agriculture-ireland-blog/climatepolicyforruminantagricultureinirelandblog7/.

See https://libguides.ucd.ie/academicintegrity on how to cite in other formats.

Update: Frank Convery received a very helpful correction to this blog on New Zealand Climate Policy for Agriculture Forestry and Land Use (AFOLU) from Madeline Hall which is included in a revised version, which clarifies the NZ government’s decision in regard to the allowability of using carbon removed by ‘permanent’ exotic forests as offsets in the NZ Emissions Trading Scheme. This is reflected in the second paragraph in the ‘Treasury Regulatory Assessment’ section below and have updated the publication data in the APA citation.

“Ireland will become a world leader in Sustainable Food Systems (SFS) over the next decade. This will deliver significant benefits…and will also provide the basis for the future competitive advantage of the sector”.

Food Vision 2030 [1]

“Success has always been a great liar.”

Nietzsche

Some Key Points

China is New Zealand’s dominant customer, buying in 2021/22 41,40 and 37 per cent of its dairy, beef and veal, and lamb exports respectively. In second place as purchasers of: dairy is Australia (5%), beef the US (32%); lamb the EU (20%). The UK is also a significant customer for lamb (11% of NZ’s exports). The carbon competition, i.e., future CO2e emissions per Kg of product, and how it is framed, that NZ will face in the short and medium term will be determined largely by China, but its exposure to the US, EU, and UK (and perhaps in time Australia) could be significant.

If New Zealand delivers a significant levy on greenhouse gas emissions and this is applied as proposed to all ruminant farms above a certain size, this could be a game changer for both New Zealand and the world. Pasture-based ruminant farming needs a climate champion. If, as seems likely, the prices that apply to emissions’ reduction and carbon removals in NZ from now to 2030 are too low on their own to incentivise emissions reduction and carbon removal at scale, then the subsidies applied to support farmers to make the transition need to be carefully designed and delivered to maximize the prospects of global leadership (more on this in Blog 12) as does its innovation strategy (Blog 11). A partnership anchored by NZ-IRL could help deliver global carbon-footprint leadership for pasture-based farming.

Introduction

Exports of dairy, beef and lamb make a hugely important contribution to New Zealand’s merchandise exports, and to the economic vitality of its rural regions. Food and fibre exports from NZ in the year ending March 2022 accounted for 80% of the country’s merchandise exports. Exports from ruminant farming – mainly dairy (NZ$21.481 billion), beef and veal (NZ$4.338 billion) and lamb (NZ$3.449 billion - accounted for over half. The issue arises as to the extent, if any, that consumers in the futures in these markets will take account of the carbon footprint of NZ’s products in making their choices, and/or the main importing jurisdictions will use their own climate policies to require performance labelling and perhaps impose some form of border tax adjustment to ensure that high performance standards are met. In , and I sketched what this could mean for Irish exports into their top three markets. In this blog under ‘Markets’ I address this issue as regards NZ.

New Zealand has devoted a lot of effort to engaging with key stakeholders to think through what sort of climate policies for the sector are both compatible with NZ ways of thinking and doing generally and could deliver emissions reduction and carbon removal at scale. It is clear from these efforts that there is a very high premium placed on securing buy in by the key stakeholders, that market led approaches are the policy instruments favoured to address the challenge, and that the latter could be an important contribution by NZ globally to finding ways that work to deliver outcomes at scale for pasture-based farming.[2]

Under ‘climate policy’ I address New Zealand’s considerable endowments, and the evolution to this point of climate policy for agriculture forestry and land use.

Markets[3]

Ruminant farming exports from New Zealand in 2021 came to 26.545 billion NZ$ (~€15.9 billion[4]), which is about twice the level of Ireland’s ruminant exports in the same year. These increased by ~33% since 2015, with much the increase in absolute value due to the rise in the value of dairy exports, which in 2021 accounted for 71.9% of the total.

Table 1. Ruminant (Dairy, Beef, Sheep) Exports, New Zealand, 2015-2021, Million NZ$

|

Product |

ROW |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

|

|

|

|

|

|

|

|

|

|

Value |

% |

|

Dairy |

(1) |

14,050 |

13,289 |

14,638 |

16,665 |

18,107 |

20,135 |

19,093 |

71.9 |

|

Beef and Veal |

(2) |

2,980 |

3,096 |

2,706 |

2,943 |

3,324 |

3,811 |

3,587 |

13.5 |

|

Lamb |

|

2,504 |

2,569 |

2,441 |

3,018 |

3,227 |

3,331 |

3,167 |

|

|

Mutton |

|

418 |

419 |

417 |

575 |

576 |

643 |

698 |

|

|

Total Sheep |

(3) |

2,992 |

2,988 |

2,858 |

3593 |

3,803 |

3,974 |

3,865 |

14.6 |

|

Total Enteric* |

(1)+(2)+(3) |

20,022 |

19,373 |

20,202 |

23,201 |

25,234 |

27,920 |

26,545 |

100 |

*Dairy, Beef and Sheep only (excluding venison, wool, hides and by-products etc.)

Source 1 (2015-2017) Ministry for Primary Industries, 2020. Situation and Outlook for Primary Industries, December. Situation and Outlook for Primary Industries (SOPI) December 2020 (mpi.govt.nz) Dairy: p.4; Beef Veal and Sheep: p. 18

Source 2 (2018-2021): Ministry for Primary Industries, 2022. Situation and Outlook for Primary Industries, June Situation and Outlook for Primary Industries (SOPI) June 2022 (mpi.govt.nz) Dairy: p. 34; Beef Veal and Sheep: p. 48

Dairy Exports

In 2021/22, four destinations accounted for 57% of dairy exports, but China (42%) dominated (Table 2), while Australia and the US together are buying 9% of NZ’s total dairy exports. As noted in Blogs 3, 4 and 5 the EU, UK and US markets account for almost 70% of Ireland’s ruminant exports, and all three have large numbers of local producers. What they do on the market side, e.g., mandatory carbon footprint labelling per kg of product, and on the supply side, e.g., reducing emissions and removing carbon at scale, could pose a strategic threat if Ireland’s abatement and removal performance falls behind theirs.

Table 2 Export Destinations in Year to March 2022, New Zealand Dairy Million NZ$

|

Destination |

Value |

% Total |

|

China |

8,727 |

41 |

|

Australia |

1,020 |

5 |

|

Indonesia |

889 |

4 |

|

US |

839 |

4 |

|

Japan |

782 |

4 |

|

Total |

12,257 |

57 |

|

GRAND TOTAL |

21,481 |

100 |

Source: Situation and Outlook for Primary Industries (SOPI) June 2022 (mpi.govt.nz) pp. 36, 37

Beef and Veal Exports

The potential for importing jurisdictions to accelerate their own performance is higher in the case of Beef and Veal where the US already accounts for 32% of NZ’s exports (Table 3) and even more so in the case of Lamb, where the EU, UK and US already buy 46% of total exports (Table 4).

Table 3. Top 5 Export Destinations, Year to March 2022 Beef and Veal, New Zealand, Million NZ$

|

Destination |

Value |

% Total |

|

China |

1,735 |

40 |

|

US |

1,388 |

32 |

|

Japan |

304 |

7 |

|

Taiwan |

174 |

4 |

|

South Korea |

174 |

4 |

|

Total |

3,775 |

87 |

|

GRAND TOTAL |

4,338 |

100 |

Source: Situation and Outlook for Primary Industries (SOPI) June 2022 (mpi.govt.nz) For Total Value p. 50 and for % of Total p. 51

Lamb Exports

Table 4. Top Six Destinations, Year to March 2022, Lamb, New Zealand Million NZ$

|

Destination |

Value |

% Total |

|

China |

1,276 |

37 |

|

EU |

690 |

20 |

|

US |

517 |

15 |

|

UK |

379 |

11 |

|

Canada |

138 |

4 |

|

Japan |

103 |

3 |

|

Total |

3,103 |

90 |

|

GRAND TOTAL |

3,449 |

100 |

Source: Situation and Outlook for Primary Industries (SOPI) June 2022 (mpi.govt.nz) For Total Value p. 50, and for % of total p. 51

On May 31, 2022, courtesy of Beef+Lamb New Zealand, I had the pleasure of visiting with Mark Guscott, at his family farm in the Wairarapa in the Southern part of New Zealand’s North, and other farmers:

"We aim to produce high quality lamb at the highest standards possible. Our whole business revolves around this principle and we've done this for many generations…. We’re trying to do this by aiming at premium markets with customers who value the same principles that we do."

Mark supplies Atkins Ranch[5], a premium lamb processor and exporter that supplies Whole Foods, a US based international supermarket chain targeting high value consumers who demand rigorous animal welfare and environmental standards. I was struck by their practical idealism – a real ‘learning by doing’ commitment to find ways that work to farm in harmony with nature, to convert this learning into outcomes, and to find ways that work to convert this to commercial advantage, epitomized by their success in getting their lamb products onto the shelves of Whole Foods: this is a boutique grocery store in the US with an annual turnover of ~$16 billion[6] which is famously careful only to stock product that is sustainable, and charges accordingly. For a relatively small cluster of farmers (~100) in NZ to secure a presence in this incredibly discerning marketplace is a huge achievement.

Climate Policy[7]

The Endowment

New Zealand has enviable endowments when it comes to addressing climate change. these include a lot of renewable energy that is commercially competitive with fossil fuels, and a capacity to remove large volumes of carbon quickly.

Renewables

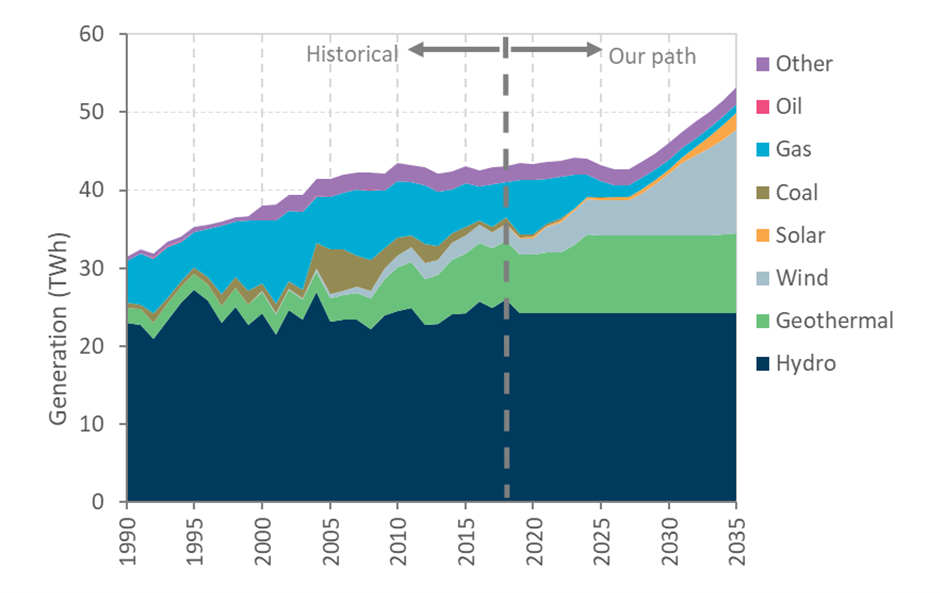

Figure 1 shows the current energy mix by fuel source, with renewables (hydro, geothermal and wind) already dominating the supply, and wind expected to provide most of the growth from now to 2035. Then we read (p. 61) “The New Zealand Aluminium Smelter is the single largest consumer of electricity. Over the last 5 years it used on average around 13% per year of the country’s electricity. In our path the smelter closes gradually, coming to a full close in 2026”.

Figure 1. Fuel Sources for Power Generation in NZ from 1990

Carbon Removal

Another source of envy is the reality and potential of New Zealand’s forests to store carbon, including especially the choices New Zealand have to ‘turn on’ very short rotation commercial forestry (mainly Radiata Pine) and/or much slower growing native forests to remove carbon at scale. The Commission envisaged a scenario where carbon removals initially dip below the 2018 level of 9.5 million tons in 2018 to allow for rise in slower growing native species, but by 2035, they see removals rising to 14.5 million tons (Table 5). The dip in 2025 would be a product of increasing the planting of slower growing native species, which is what the Commission recommends.

Table 5. Current and Projected Carbon Removal by Forestry, New Zealand, 2018-2035, MT CO2e

|

|

2018 |

2025 |

2030 |

2035 |

|

|

|

|

|

|

|

Total Forestry |

-9.5 |

-6.1 |

-10.7 |

-14.5 |

Source: Climate Change Commission, 2021. 2021 Advice for Consultation, New Zealand, January 30, page 57.

The Core Climate Challenge

In contrast to these advantages is the fact that emissions from agriculture in 2018 totalled 37.8 million tons of carbon dioxide equivalent, comprising 48 per cent of total emissions (78.8 million tons). As we have seen, ruminant farm output accounts for around 50 per cent of New Zealand’s merchandise exports, and these sell into highly competitive global markets. As part of its economic reforms in the 1980s, subsidies to farming in NZ were virtually eliminated, so this policy instrument was not readily available. This reality, combined with what is now a cultural pre-disposition for market solutions, led to the adoption of emissions trading.[8]

Evolution of Climate Policy

An overarching context is that agricultural emissions are legislated to enter the Emissions Trading Scheme by 2025. The government can bring them in sooner if it believes that the He Waka Eke Noa partnership (see below) has made insufficient progress in preparing the farming sector for farm-level emissions pricing.

Biological Emissions Reference Group (BERG)

In December 2018, an important document - Report of the Biological Emissions Reference Group (BERG) which was set up in June 2016 - was published.[9] Its importance derived from the following:

- Its membership: comprising government (Ministry of Primary Industry, and Ministry of Environment), farm organizations and industry (Beef + Lamb New Zealand, Dairy New Zealand, Deer Industry New Zealand, Federated Farmers of New Zealand, Fertiliser Association, Fonterra, Horticulture New Zealand).

- Its brief: to ‘build a portfolio of evidence’ that identified both the opportunities to reduce biological greenhouse gas emissions from New Zealand agriculture (methane and nitrous oxide), both today and in the future and the costs and benefits of these mitigation opportunities, and any barriers to their use.

- Their evidence was marshalled from credible sources: AgResearch, Manaaki Whenua – Landcare Research, the New Zealand Agricultural Greenhouse Gas Research Centre, Beca Group, AgFirst, and Motu - and subjected to peer review.

- It tells us how long it takes a such a stakeholder group to produce a report – 2.5 years from set-up in June 2016 to report publication in December 2018.

In the assessment of scenarios (Chapter 4.4) the report flags the already existing NZ ETS and uses prices per ton of C02e sequestered or reduced to assay implications – see ‘Table 7: Four scenarios of prices for greenhouse gas emissions produced on farms, for 2012, 2030 and 2050’ p. 44.[10]

Interim Climate Committee

This inclination is reflected in New Zealand’s Interim Climate Committee report, 2019, where chapters 6, 7 and 8 are devoted to issues around pricing. In chapter 8, it assesses three pricing models: Including agricultural emissions in the New Zealand Emissions Trading Scheme (NZ ETS); A dual cap ETS or methane quota system; levy/rebate scheme for agricultural emissions.[11] They conclude (p. 69) as follows:

“If livestock emissions are priced at the farm-level, then a levy/rebate scheme is the best way to enable that. This will reduce the cost, complexity and risk for farmers that would come with trading units in the NZ ETS, dual cap ETS or a methane quota system, and won’t affect cost-effectiveness or New Zealand’s ability to manage the transition toward long-term targets”.

In its recommendations on climate budgets and the direction of policy (Chapter 6) needed to achieve them, the current climate commission advised (p. 104)

- Emissions pricing and other market incentives to influence choices.

- Regulation education and other action to address barriers.

- Investments in technology, infrastructure to spur innovation and system transformation

As regards the first of these it suggested that:

“Drawing on the work of He Waka Eke Noa (Primary Sector Climate Action Partnership), decide in 2022 on a pricing mechanism for agricultural emissions as is required by legislation that is suited to the characteristics of the sector and capable of supporting achievement of the emissions budgets and targets”.

As regards innovation, it is interesting to note that BioTech’s CALM (Cut Agricultural Livestock Methane) programme has secured nearly $8 million from the state. Ruminant BioTech investors will match the Crown’s cash injection. The company aims to develop a commercially viable bolus by 2025 that delivers at least a 70% reduction in ruminant animals’ methane emissions over six months.[12]

He Waka Eke Noa (Primary Sector Climate Action Partnership)[13]

In addition to the stakeholders represented in the BERG work, the Māori had a seat at this table. The partnership was given status and responsibility on October 2019, when the government agreed to a proposal from the primary sector to work together and with iwi/Māori to develop a system for measuring managing and reducing agricultural greenhouse gas emissions, rather than simply putting farm products in the ETS. About 2.5 years after it was given its mandate, the final recommendations were released on 31st May 2022. They were as follows:[14]

- Farms calculate their short- and long-lived gas emissions through a single centralised calculator (or through existing tools and software that are linked to the centralised calculator).

- Calculated on-farm emissions determine the levy cost rather than the use of national averages.

- Recognition of reduced emissions from on-farm efficiencies and mitigations as they become available.

- Incentives are provided for uptake of actions (practices and technologies) to reduce emissions.

- A split-gas approach applies different levy rates to short- and long-lived gas emissions.

- On-farm sequestration is recognised, which could offset the cost of the emissions levy.

- Levy revenue is invested in research, development, and extension (providing technical advice and information) including a dedicated fund for Māori landowners.

- A System Oversight Board with expertise and representation from the primary sector, will work closely with an Independent Māori Board to provide recommendations on levy rates and prices, and set the strategy for use of levy revenue.

The Partners consider the recommended system to be a ‘practical, credible, and more effective alternative to pricing agricultural emissions via the NZ ETS. Levy rates need to be as low as possible while still achieving the objectives of reducing emissions, increasing integrated sequestration, and minimising impacts on primary sector production and profitability’.

The Climate Change Commission

The Climate Change Committee supported the proposal, reflected in the words of its chair, Rod Carr:[15]

- "The best approach to pricing agricultural emissions would be a detailed farm-level pricing system outside the NZ ETS. This system would be best able to recognise and reward the good choices farmers make to reduce their gross emissions in line with the statutory targets,"

- With significant effort - implementing a basic farm-level system, using a streamlined version of the He Waka Eke Noa proposal, would be possible by 1 January 2025. This will rely on the necessary IT systems being designed and built, compliance and enforcement functions established, and regulations put in place.

- Our actions in Aotearoa New Zealand matter. We will be the first country to design agricultural emissions pricing, and globally all eyes will be on what that looks like and how it works.”

Recent Developments

The government then produced: its response to the He Waka Eke Noa report, in the form of tabling recommendations on pricing emissions (levy), on which feedback was sought; its recommendations as regards the qualification of owners of exotic forests for payment per ton of CO2 removed via NZ ETS; these were followed in December 2022 by its decisions on pricing emissions, and by the Treasury’s regulatory impact assessment of planting exotics and generation of NZUs in ETS.

Government Proposals on Pricing Greenhouse Gas Emissions from agriculture in NZ: In October 2022, the government proposed as follows:[16] From 2025 New Zealand proposes to apply a levy on greenhouse gas emissions with the following features: participation will be obligatory for all farms with 50 or more dairy cattle, or >550 stock units (deer, sheep, cattle) or who apply 40 tonnes or more of synthetic nitrogen. Emissions must be reported to the Emissions Trading Register. Levy payable [(Kg methane emissions x levy rate) + Kg long lived gasses (N2O, CO2) x long lived levy rate]. Incentive payments for approved mitigation technologies and on-farm vegetation. Levy rate for: long lived gasses will be linked to the unit prices in NZ ETS; methane – Climate Change Commission to advise ministers. Use of levy revenues developed with Māori/sector advisory body/bodies – fund incentive payments, administration and research and development. This consultation ends on 18 November 2022. Once submissions have been considered, final proposals will go to ministers for approval in early 2023.

Government Action on Pricing GHG emissions (and carbon removals) from agriculture in NZ. In December 2022, the government published the specifics of its pricing proposals.[17] Fifteen features are listed, including that that participation will be obligatory for farms registered for VAT who meet the emissions thresholds (equivalent to ~200 tonnes CO2-e per year)

If this threshold applied in Ireland, it seems likely that most dairy farms would be included as would ~40% of beef and sheep farms.

Table 6. Greenhouse Gas Emissions, Average Farm, by Farm System, tonnes of CO2e, Ireland, 2021

|

Farm System |

GHG Emissions tonnes of CO2e |

|

Dairy |

614.1 |

|

Beef |

156.6 |

|

Sheep |

166.0 |

Source: 2021-Sustainability-Report.pdf (teagasc.ie), pp.78, 80, 82.

Farmers can choose to be monitored and to report as a group, and payments will be available to reward the uptake of incentives and eligible sequestration (removals). The most significant change from the earlier proposals is that it is proposed that relatively low, unique prices could be set initially for both biogenic methane and nitrous oxide for five years based on set criteria and payments would be available to reward the uptake of incentives and eligible sequestration (removals). This change means that emissions up to 2030 are likely to be higher than they would have been if higher prices were applied, and this could have implications for the carbon-competitiveness of NZ ruminant output.

Proposals to end linkage between planting of exotics and generation of NZUs in NZ ETS:[18] The success of New Zealand’s climate strategy depends significantly on carbon storage by trees. It is estimated that, as a result of past grant schemes, forest planting will sequester 46 million tonnes of carbon dioxide from 2022 to 2035. Without any restrictions on area or species planted, a new scheme was introduced in the Climate Change (Emissions Trading Reform) Amendment Act in 2020, scheduled to open for registrations from 1 January 2023 whereby landowners who plant a permanent forest can earn and then sell or use tradeable units (New Zealand Units or NZUs) within the scheme based on the amount of carbon their forest removes from the atmosphere. Allowance prices per unit (NZU ARE tons of CO2) in NZ ETS has more than doubled within the last year, from around NZ$35 in late 2020 to upwards of NZ$80 in early 2022.

The government has identified a number of issues with this policy which include: large areas of land nationwide (relative to historic trends) being planted in permanent forests consisting of exotic species (mainly radiata pine) which are not intended to be harvested; increase in the supply of NZUs to the NZ ETS from these forests is likely to dampen medium-term carbon prices in the NZ ETS; The Climate Change Commission identified a clear role for indigenous afforestation which provides slower but sustained sequestration throughout this century.

It proposed the following:

“Given these risks, we propose to remove the ability to register exotic species within the permanent forest category of the NZ ETS. This would mean that forests that consist of exotic species (such as Pinus radiata, other conifers, or hardwoods) would not be eligible to be registered as a permanent forest.”

Treasury Regulatory Assessment: In its assessment of the choices released in December 2022, the Treasury’s regulatory impact assessment notes that “Option 3: legislation to restrict the permanent forest category to indigenous forests but allow some exotic forests under certain circumstances is MPI and MfE’s preferred option. This option best manages risks of displacement of farming and production forests, and long-term risks to NZ ETS market conditions and environmental risks. This option allows for permanent exotic forests where these can realise positive outcomes (such as to the local environment, communities, economic returns from otherwise unproductive land and to support Māori land aspirations).”[19]

However, the NZ government decided not to accept this ‘preferred option.’ See a link here to a plethora of government documents outlining officials’ recommendations and government’s decision. Note that the decisions only related to the limiting of exotics in the ‘permanent forest’ category of the NZ ETS and not the wider use of forestry offsets in the scheme. I am very grateful to Madeline Hall, Beef + Lamb New Zealand, for bringing this decision to my attention, which was omitted from the earlier version of this Blog, and for providing the link to the relevant documentation.

Assessment

Markets

- In its main markets, and especially China, NZ does not yet face the likelihood of locally decided independent carbon performance labelling and the potential for carbon border adjustment mechanisms that would favour the best performers.

- Mark Guscott and the other farmers who supply Atkins Ranch show that when NZ farmers roll up their sleeves and commit to sustainability they can compete with the best in the world and find ways to convert it into market advantage.

- However, in the spirit of Andy Grove, CEO of Intel (‘only the paranoid survive’),[20] NZ needs to be paranoid about what the competition could get up to in the future; it already has some exposure to jurisdictions that have the potential reduce emissions at scale, with 9% of dairy exports already going to Australia and the US, 32% of beef to the US, and 20% of lamb to the EU.

- China is already imposing increasingly demanding emissions standards on all new cars sold in its market. In the medium term, it could extend this approach to food.

Climate Policy

- The BERG and He Waka Eke Noa recommendations together took 5 years from set up to delivery. If NZ moves on to design and deliver policies that deliver emissions reductions and carbon removal at scale, posterity will regard this considerable time investment as well worthwhile. If not, posterity’s judgments will be less kind.

- If, as the government has proposed, NZ introduces pricing for emissions and makes participation obligatory for farms above a certain size threshold, these will both be unique contributions – no one else has yet embraced this twin approach; in time it could revolutionize performance globally.

- It will succeed if: farmers have information on emissions and choices that are good enough to justify rewarding them; prices that are sufficiently high to incentivize reduction of emissions and storage of carbon at scale; an innovation strategy is in place that drives finding ways that work at scale to reduce enteric methane emissions from grass-fed systems (see Blog 11); and a portfolio of supports that are efficiently administered that help to reduce emissions and remove carbon at scale.

- If, as seems likely, from now to 2030 the prices that are applied to nitrous oxide and methane emissions, and to carbon removal, are too low to on their own to ensure global carbon-footprint leadership for N.Z.’s grass fed ruminant farming, it is important that the subsidies that are available to farmers are designed and delivered to maximize the prospects of such leadership (see Blog 12) for ideas in this regard.

- Australia could be the surprise. When the Irish Nobel Prize winning writer Samuel Beckett was asked by a French journalist if he was English, he replied ‘Au contraire’. When New Zealanders are asked by foreigners if they are Australian, I have noted that many reply in the same spirit, albeit at times with less elegance but more vehemence. With a record of great innovation as regards solar energy,[21] and considerable experience with creation of water markets,[22] there is a lot of pent-up ambition and talent in Australia that has been frustrated and held back by profoundly incompetent climate policy at federal level. This now seems to be changing, and if it does, Australia could address climate policy for agriculture with great clarity speed and effectiveness.

- The rapid response at scale by investors to the opportunity provided by the returns available from the market (NZ ETS) to plant exotics that permanently store carbon is notable. Ireland is depending on generous grants (direct subsidies) and tax expenditures (tax breaks for companies and individuals) to deliver carbon storage outcomes at scale, and the same challenges faced by NZ – namely deciding on the balance between native and indigenous species, and how to deliver this – arise.

- Finally, the world badly needs a climate change champion for pasture based ruminant farming, and anchoring this by a deep NZ-IRL collaboration could deliver it: There are already enabling mechanisms in place;[23] they are both tiny actors on the world stage, but happen to have a major position in some of the world’s key markets which creates both vulnerability and opportunity; in both cases, the economic and social vitality of their rural economies in the medium term will depend significantly on the global competitiveness of their carbon footprints most of the technical solutions emerging for enteric methane abatement may be best suited on a cost-effective basis to indoor containment systems – we have a shared interest in making sure that pasture fed systems do not fall behind. BioTech’s CALM initiative, whereby $16 million is dedicated finding such a path forward, may symbolize the beginnings.

Header image credit: Photo by James Coleman on Unsplash

« Climate Policy For Ruminant Agriculture In Ireland blog series

How to cite this blog (APA): Convery, F. (2023, January 27). Climate Performace by Irish Ruminant Farming: New Zealand Climate Policy for Agriculture Forestry and Land Use (AFOLU). UCD Earth Institute Climate Policy for Ruminant Agriculture in Ireland. https://www.ucd.ie/earth/newsevents/climate-policy-agriculture-ireland-blog/climatepolicyforruminantagricultureinirelandblog7/.

Biography

Frank Convery has degrees [B. Ag and M.Ag (Forestry)] from UCD. Encouraged by the late Seamus Sheehy, he went to the US and took a PhD in Forestry Economics (State University of New York). After a distinguished academic career in the US (Duke University) he returned to Ireland as research professor at ESRI before being appointed as Heritage Trust Professor of Environmental Studies at UCD where he led the successful application for the funding of the UCD Earth Institute. He chaired the boards of the Sustainable Energy Authority of Ireland (SEAI) (2002-2007), Comhar Sustainable Development Council (2006-2010) and served on the Climate Change Committee (2016-2020) chaired by John FitzGerald, and the AgriFood 2030 Committee chaired by Tom Arnold. The latter produced Food Vision 2030. From 2014 to 2018, he was chief economist with the Environmental Defense Fund, New York. His passion is finding ways to bring the weight of learning down to where things are done; his ambition for the sector is the same as Food Vision 2030’s: “Ireland will become a world leader in Sustainable Food Systems (SFS) over the next decade. This will deliver significant benefits…and will also provide the basis for the future competitive advantage of the sector”.

Footnotes and references

[1] gov.ie - Food Vision 2030 – A World Leader in Sustainable Food Systems (www.gov.ie) p.9

[2] Australia may also decide to lead in this space. See Final Report - Action on the land (climatechangeauthority.gov.au) April 2018 on the creation of markets and opportunities (pp. 30-38) and the Emissions Reduction Fund (pp 43-44) for intimations in this regard.

[3] Note that the data on the value of ruminant farming in NZ is an understated, because it excludes many products, including venison, wool, hides and by-products etc.

[4] I use a conversion rate of €0.60 per 1.00 NZ$, recognizing that this varies

[6] Whole Foods Market - Statistics & Facts | Statista

[7] A lot of the data text and insights in this section draws from: the NZ Climate Change Commission’s Draft Advice for Consultation submitted to the government January 31 2021 CCCADVICETOGOVT31JAN2021pdf.pdf (climatecommission.govt.nz) Page numbers cited immediately below are from this; my feedback thereon submitted March 28 2021 ID ANON-NZPP-DFSB-7, and my presentation to the Commission’s international speaker series, April 8, 2021. Meetings in Wellington in June 2022 with: MPs; staff at Ministry for Primary Industries; members and staff of the NZ Climate Change Commission; Parliamentary Commission for Environment; field trip to cattle and sheep farmers organized and hosted by Beef+Lamb New Zealand. Also, over some years, seminars hosted by MOTU. The interpretation of what I have read, seen and heard is my responsibility alone.

[8] See: A-Guide-to-the-New-Zealand-Emissions-Trading-System-2022-Update-Motu-Research.pdf

[9] Report of the Biological Emissions Reference Group (BERG) (mpi.govt.nz)

[10] New Zealand had considerable experience in the use of markets to improve the management of biological resources. See The_adoption_of_market-based_instruments_for_resou.pdf for a discussion on its performance with ocean fisheries

[11] Interim Climate Change Commission Report, 2019. FINAL ICCC - Embargoed - Action on Agricultural Emissions report.pdf

[12] https://www.ruralnewsgroup.co.nz/dairy-news/dairy-farm-health/methane-inhibitor-bolus-could-reduce-emissions-by-70

[13] He Waka Eke Noa - Primary Sector Climate Action Partnership

[14] FINAL-He-Waka-Eke-Noa-Recommendations-Report.pdf (hewakaekenoa.nz) p. 5

[15] Farmers could be ready for 'basic' emissions pricing by 1 January 2025 » Climate Change Commission (climatecommission.govt.nz)

[16] Ministry for the Environment and Ministry for Primary Industries. 2022. Pricing agricultural emissions: Consultation document. Wellington: Ministry for the Environment, October. Pricing-agricultural-emissions-consultation-document.pdf (environment.govt.nz), p.19

[17] Ministry for the Environment, Ministry for Primary Industries, NZ Government, 2022: Pricing agricultural emissions, December 22. Summary pp. 4-5. Pricing-agricultural-emissions-report-under-section-215-of-the-CCRA.pdf (environment.govt.nz)

[18] Ministry for Primary Industries. 2022. Managing exotic afforestation incentives: A discussion document on proposals to change forestry settings in the New Zealand Emissions Trading Scheme. Wellington: Ministry for Primary Industries Managing exotic afforestation incentives (mpi.govt.nz) pp. 5-8

[19] Treasury, The, 2022. Regulatory Impact Statement: Managing Permanent Exotic Afforestation Incentives, December 5. Regulatory Impact Statement: Managing Permanent Exotic Afforestation Incentives - 1 September 2022 - Regulatory Impact Statement - Ministry for Primary Industries (treasury.govt.nz), p.8

[21] I tell this story in Convery FJ (2021). Carbon-reducing innovation as the essential policy frontier – towards finding the ways that work. Environment and Development Economics 1–20. https://doi.org/10.1017/ S1355770X20000467

[22] Australian Water Markets Report 2020–21 (bom.gov.au)

[23] Statement on Joint Cooperation in Agriculture between Ireland and New Zealand | Beehive.govt.nz and https://globalresearchalliance.org/country/ireland/