Should we put a price on nature? Would we be able to afford the ambitious restoration goals now being set at an EU-level without commodifying restoration? In the following blog, Dr Shane Mc Guinness of the School of Architecture, Planning and Environmental Policy (UCD) takes a closer look at the investment potential for conservation, and how we might go about carefully tapping into this vast resource.

Clara Bog, Co. Offaly. Peatland restoration offers an increasingly strong “investible proposition”, through climate mitigation, carbon sequestration, community benefit and biodiversity gain. This requires verification, monitoring and meaningful community engagement. Credit: National Parks and Wildlife Service.

The loss of biodiversity is now one of the most pressing concerns of governments, businesses and private individuals around the world. Not only is this importance linked to a moral imperative to conserve biodiversity, but also the increasingly recognised economic value of biodiversity as a commodity unto itself. Further, the potential for biodiversity to offset the effects of human-induced climate change is now well-founded. These so-called ‘nature-based solutions’, encapsulated within a broader sustainability narrative, are now firmly in the lexicon of politicians, business-people and wider society. Indeed, the Dutch Central Bank recently declared that biodiversity loss is now a tangible economic risk to the Netherlands, threatening up to 36% of assets.

However, we are far from residing in a socialist utopia, where risk is rationalised, non-exclusive benefits are shared and the costs of improving the lot of future generations are equally divided. Until such a time, we must increasingly rely on the prevalent neo-capitalist model (which underpins even the most left-leaning societies of today) to achieve our biodiversity conservation goals. In other words, for the time-being, money matters.

Making nature pay its way, a form of ‘green developmentalism’, is now a given, by identifying the benefits provided by a species, ecosystem or process, boiling this down to a ‘flow’ and placing a value on this provision. Indeed, the concept of natural capital accounting relies on this simplification. This necessity to attribute economic value is particularly true given the over-reliance on extremely limited grant funding for restoration or the role of philanthropy, which in itself often has ulterior legacy-modification motives at play.

The good news is that those with the funding to help are increasingly willing to spend real money on biodiversity, whether aimed at offsetting future fines or costs (transitional risk), strengthening the appearance of their entity (reputational risk), or simply appearing more ethical on the surface (green washing). In most cases, these funds require some form of return-on-investment (RoI), where initial capital provides the liquidity to generate a green return, be that through commodity production, generation of carbon credits, or offsetting other costs such as water treatment. Additionally, finance offered by States (e.g. Irish Sovereign Green Bond), or larger continent-wide mechanisms (e.g. European Investment Bank) is often termed concessional finance, where the interest rate on loans is very low and expectations for RoI are also kept minimal.

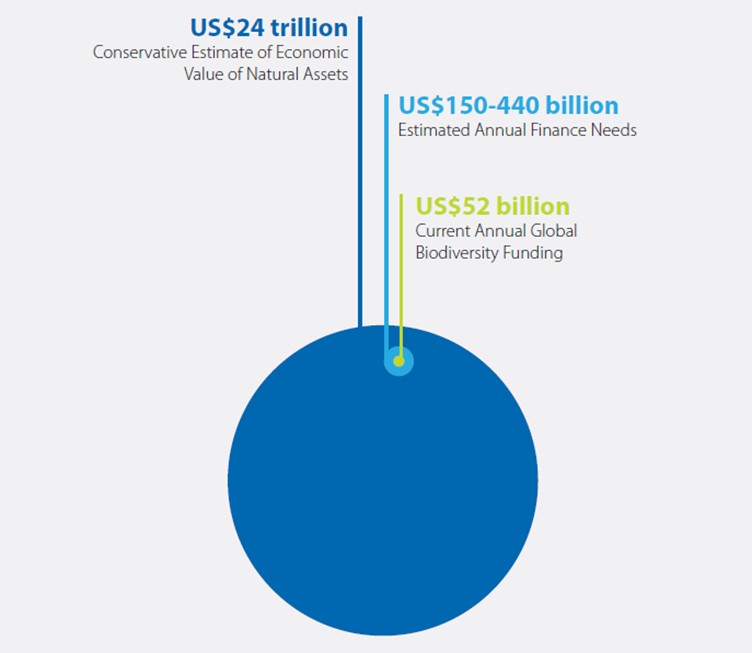

Natural capital provides us with far greater value than the investment required to maintain it, which itself also far exceeds the actual investment currently in its protection. Credit: Global Canopy Programme, 2012 and BIOFIN, 2018.

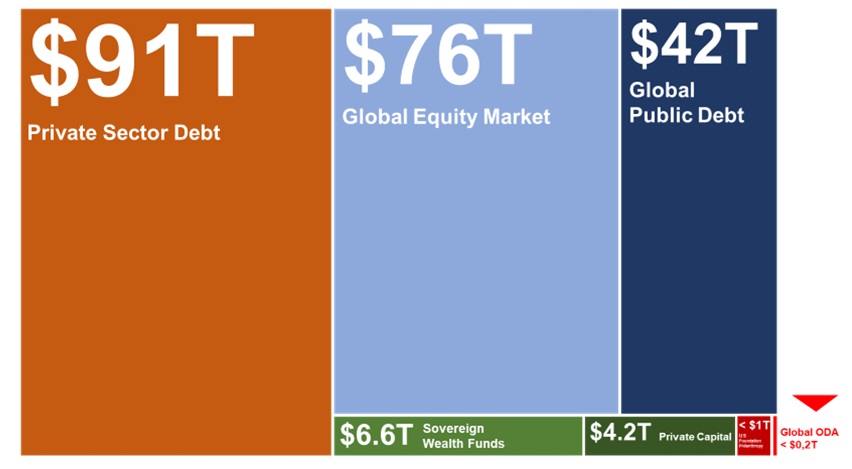

For Green Bonds, it is though that there is now upwards of $1 trillion available globally for investments deemed to be green. However, even though the scale of this finance is much larger than direct grants, it still pales in comparison to the wider global investor pool, who are not necessarily green in nature but would invest if the right motivations were present. This wider investor pool is astronomical in scale, and includes sovereign wealth funds ($6.6T), global public debt ($42T) and private sector debt ($91T). As low-hanging fruit within this, impact investors, though still holding a strong capitalist mentality, want to be sure that their accumulated, concentrated wealth does as much good as possible. The trick here is displaying confidence in your system, with science-based assumptions and targets, and having a good story that appeals to what may ultimately be the decision of a small handful of board members.

One of the best ways of appealing to these upper echelons of conservation finance is to think big. Not just species, habitats or ecosystems, but entire landscapes, which offer a diverse, robust and resilient ‘bundle’ of ecosystem services. By offering this diversified portfolio of natural assets, and funding it through blended finance (private, government, commercial, etc.), these landscape-scale investment plans are generating verified biodiversity and climate gains, while improving incomes for communities and returning profits (albeit smaller than other, less ethical investments).

Total global investor pools, showing the potential for return-based investment if a viable and trustworthy return on nature investment can be proposed. Almost all nature investment at present resides in the small red square at bottom-right. Credit: Landscape Finance Lab.

Total global investor pools, showing the potential for return-based investment if a viable and trustworthy return on nature investment can be proposed. Almost all nature investment at present resides in the small red square at bottom-right. Credit: Landscape Finance Lab.

The timing is right for these blended investment plans. Corporations in particular are now under pressure from shareholders to ensure that activities and investments are seen to have good environmental, social and governance criteria at their core. These so-called ESG metrics are a strong driver for landscape-level finance for conservation. Further, companies will soon be required to account for their environmental impact and tangibly act to reduce this. For example, National carbon emissions are already well understood, with ambitious targets set for reduction. These same requirement are soon likely to be part of the private corporate landscape too, and investors know this. As such, biodiversity is increasingly seen as an “investible proposition”, especially if this combines climate and social benefits.

As Zimmerman succinctly noted way back in his 1951 book World Resources and Industries: A Functional Appraisal of the Availability of Agricultural and Industrial Materials, “resources are not, they become”. In other words, without the wide suite of values attributed to a species, habitat or ecosystem, their existence would remain arbitrary to humans. Biodiversity, by offering real value to businesses in various ways, is now increasingly seen as a financial asset. Woe betide investors who disregard this inexorable truth!

Essay first published 24 May 2022.

About the author

Dr Shane Mc Guinness is a Research Fellow in the School of Architecture, Planning and Environmental Policy at UCD, and sits on the Associate Members Committee of the Earth Institute. He is currently a coordinator of the WaterLANDS project, an ambitious EU Green Deal-funded project aimed at upscaling restoration of wetlands across Europe. He founded the Peatland Finance Ireland project aimed at mobilising blended finance to support peatland restoration in Ireland and recently conducted a review of the financing of biodiversity actions in Ireland. His background is conservation biology by training, specialising in human-wildlife conflict and environmental education and he is a Fellow of the Royal Geographical Society.

About the series

The A-Z of Environmental, Climate and Sustainability Research is a new series of short essays by UCD postdoctoral and postgraduate researchers, technical and research support staff, about their work. The series is developed and curated by the Earth Institute Associate Member Committee led by Hannah Gould, a PhD student at BiOrbic and the UCD School of Architecture, Planning and Environmental Policy, and Earth Institute Communications and Engagement Officer Liz Bruton. If you'd like to submit a piece for the series do get in touch!

Find out more about the Anthropocene with Nick Scroxton, Bees with Katherine Burns, Cannabis with Caroline Dowling, Degrowth with Ciarán O'Brien, Education with Georgina Fagan, Finance with Shane McGuinness, Gaia with Federico Cerrone, Hydrometry with Kate de Smeth, Innovation with Hannah Gould, Justice with Lauren Minion, Kelp with Priya Pollard, Landscape part 1 with Tomas Buitendijk, Landscape part 2 with Amy Strecker and Amanda Byer, Reusing microbial ‘bathwater’ for sustainable drug production with Laura Murphy, and Mammals with Virginia Morera-Pujol in our latest essays.

Further reading

De Nederlandsche Bank (DNB) and PBL Netherlands Environmental Assessment Agency, Indebted to nature – Exploring biodiversity risks for the Dutch financial sector, June 2020.

Mcafee, K. 1999. Selling nature to save it? Biodiversity and green developmentalism. Environment and Planning D: Society and Space, 17, 133-154.

UN SYSTEM OF ENVIRONMENTAL ECONOMIC ACCOUNTING

Zimmerman, E. W. 1951. World Resources and Industries: A Functional Appraisal of the Availability of Agricultural and Industrial Materials, New York, Harper and Bros.